While investments in India's climate-tech sector grew significantly in previous years due to increasing interest from domestic and international investors, the funding momentum waned by the end of November 2023, reveals consulting firm FSG's new report, 'India's Green Revolution 2.0: Trends Shaping India's Climate-Tech Sector'. According to the report, the sector attracted US$ 2,853 million until November 30, 2023, representing only 57% of the total investment garnered in 2022.

FSG's analysis shows that investment activity has been driven primarily by significant funding in the'mobility' and 'energy' sub-sectors, which collectively secured over 94% of the total climate-tech investments in India from 2019 till the end of November 2023. This dominant trend underscores the critical focus on these areas within the broader climate technology field.

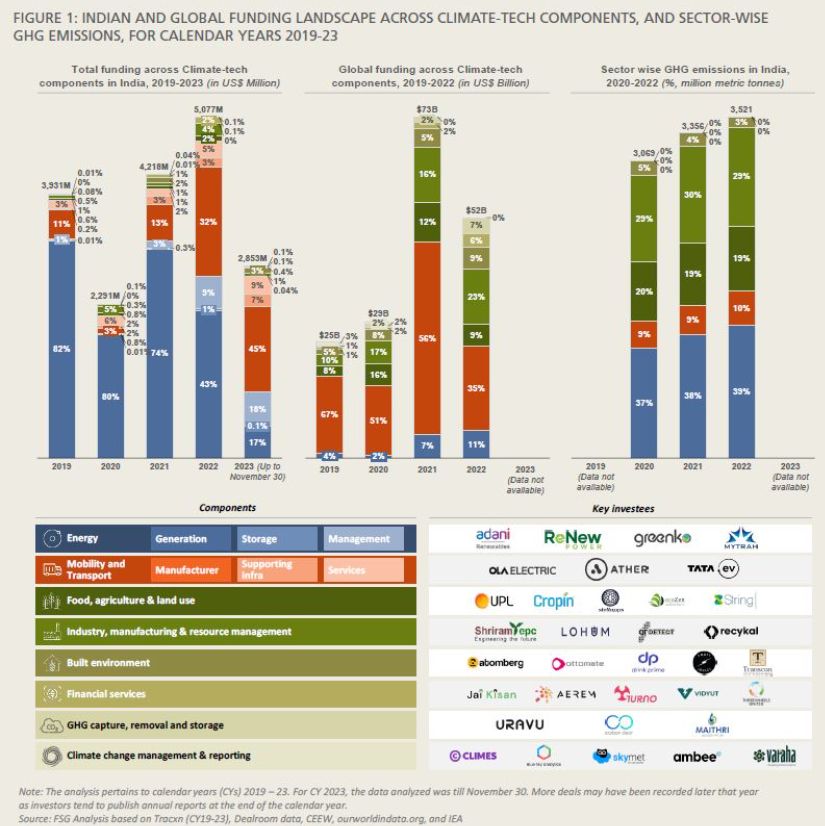

The report also highlights a dissonance between the emissions contributions of individual sub-sectors and the amount of climate-tech funding they receive. The ‘energy' sector accounts for approximately 38% of total emissions, however, it secured an outsized 74% share of climate-tech investments, on average, between 2019 and 2022.

Meanwhile, though the 'industry, manufacturing, and resource management' sector and the 'food, agriculture, and land use' sector account for approximately 30% and 20% of total emissions, respectively, they collectively received only about 4-5% of the total investments over the analysis years. To limit global warming to 1.5◦C, investors should correct this dissonance by realigning their investment focus.

FSG's report tracks the trajectory of investments in India's climate-tech sector since 2019, analysing funding stock and flows across the sub-sectors in climate-tech. Exploring emerging trends and potential business models in the sector, it also offers insight into the future outlook for each sub-sector and delves into the implications for key stakeholders such as start-ups, legacy companies, the government, and investors.

Commenting on the release of the report, Rishi Agarwal, MD, Head-Asia, said, “As India prepares for the upcoming general elections, this report couldn’t be more timely. It highlights the role climate innovation and sustainable practices play in our nation’s future, underscoring the importance of prioritizing climate solutions in our national agenda. As political parties draft their manifestos, they should incorporate policies that support and accelerate the adoption of climate-tech solutions, demonstrating a commitment to a greener and more sustainable future.”

Investment trajectory

According to the report, India's climate-tech sector attracted investments totaling US$ 3,931 million in 2019, US$ 2,291 million in 2020, US$ 4,218 million in 2021, US$ 5,077 million in 2022, and US$ 2,853 million till November 30, 2023.

It reveals that despite a temporary setback in 2020 due to the economic disruptions induced by COVID-19, which led to a 42% reduction in funding compared to 2019, India's climate-tech sector has demonstrated resilience, registering an overall funding increase of 29% from 2019 to 2022. This growth culminated in a record total investment exceeding US$5 billion in 2022, a milestone signifying a robust vote of confidence in the sector's potential for impact.

The overall investment growth in the climate-tech sector in recent years can be attributed to several key factors. 'Primarily, there has been a significant rise in awareness among citizens, businesses, and governments regarding the importance of embracing sustainable practices. Additionally, the government has steadily enhanced incentives in the sector, sparking interest among investors,' the report states.

"Despite short-term fluctuations, the long-term growth trajectory of India's climate-tech sector remains promising, underpinned by increasing awareness and government incentives. The recent decline in late-stage investments reflects a sharper investor focus on profitability. While this may cause short-term deceleration, it also indicates a maturing market where investors are seeking sustainable and financially viable solutions. The slowdown also highlights the need for climate-tech companies to demonstrate clear paths to profitability to maintain investor interest in the long term," said Agarwal.

Deep dive into sub-sectors

While the general trajectory of India's climate-tech sector shows an upward trend, there are distinct variations within specific sub-sectors, which are explored in detail in the report.

FSG's analysis shows that investment activity has been driven primarily by significant funding in the 'mobility' and 'energy' sub-sectors, which collectively garnered over 94% of the total climate-tech investments in India from 2019 until the end of November 2023.

These sub-sectors are followed by the 'industry, manufacturing, and resource management' sub-sector, garnering close to 2% of total investments over the same period, and the 'built environment' and 'food, agriculture, and land use' sub-sectors, both of which secured slightly over 1% of the total funding. The 'financial services' sub-sector received less than 1% of the total climate-tech funding.

'Greenhouse gas (GHG) capture, removal, and storage' and 'climate change management and reporting' are nascent sub-sectors that received a negligible share of the investment pie.

Emissions realities and funding disparities

According to the report, 'Aligning climate-tech investments with the need for emissions reduction in sectors contributing significantly to greenhouse gas emissions offers the potential for both environmental impact and economic growth.'

The energy sector is the largest contributor to GHG emissions in India, accounting for approximately 38% of total emissions. Between 2019 and 2022, it secured an average 74% share of climate-tech investments. 'While this outsized investment favours the energy sector, it leaves other emissions-intensive sectors lacking adequate funding', the report states.

Following closely, the 'industry, manufacturing, and resource management' sector contributes around 30% of GHG emissions, while 'food, agriculture, and land use' accounts for approximately 20% of emissions. However, despite these sectors' significant contributions to GHG emissions, they have received only a small proportion of climate-tech investments, collectively representing about 4-5% of the total investments over the analysis years.

For climate action to stay on track to limit global warming to the 1.5◦C threshold, investors should correct this dissonance by realigning their investment focus.

"The notable disparity between sectors' contributions to GHG emissions and their share of climate-tech investments underscores the urgency for strategic realignment. While investments in the energy sector dominate India's climate-tech landscape, there is a pressing need to diversify funding towards sectors like industry, manufacturing, and agriculture, which contribute significantly to emissions. This diversification will be key to achieving meaningful reductions in greenhouse gas emissions," said Agarwal.

About FSG

FSG is a global mission-driven consulting firm that partners with foundations and corporations to create equitable systems change. Through customised consulting services, innovative thought leadership, and learning communities, we're working to create a world where everyone can live up to their full potential.

Please find the full report attached here.

/articles/indias-climate-tech-funding-landscape